-

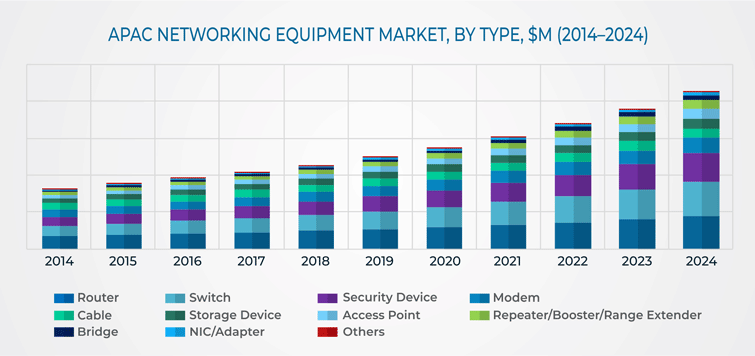

Connected Workplace has A Lot to do with the Increasing Demand for Networking Equipment in the APAC

The APAC networking equipment market will have significant growth in the years to come. This is because of the factors like increasing bandwidth requirements and mounting data traffic. Additionally, rising incidents of cyber-attacks are also pushing the demand for networking equipment where organizations are obligated to accept networking security solutions so as to alleviate risks ascending from this kind of attack.

The industry is considered into routers, security devices, switches, modems, cables, storage devices, access points, repeaters, bridges, NIC, and others including amplifiers, antennas, and hubs. Of these, routers had the maximum demand in the past. Furthermore, momentous demand for high-speed data transmission from clients has permitted large enterprises to improve network competence at reduced working costs, which will improve the growth prospects for routers in the future.

Repeaters with speeds above 300 Mbps will have the largest share in the years to come. Furthermore, the demand for these will exhibit the fastest growth in the near future. This is a result of the requirement of incessant availability of robust network and internet connectivity in administrations in addition to consumers.

An unmanaged switch will hold a larger revenue share in the near future. Though, managed switches will register faster growth in the coming years. This is a result of the fact that managed switches bid better control as compared to the data access authorization, and has the aptitude to arrange, accomplish, and monitor the LAN. The initial funding is in managed switches as opposed to unmanaged switches, but large enterprises prefer managed switches because of their improved quality of security and service.

The growing hospitality sector is posing a prospect for the APAC networking equipment market. Japan and India are posting healthy development in hospitality sector. Currently, Wi-Fi in hotels is not a luxury facility anymore. As Wi-Fi connection is a vital part of contemporary lifestyle, many guests are seeing the attendance of Wi-Fi facility as a part of their policymaking process whilst confirming reservations. Consequently, increasing the hospitality sector would surge the requirement for networking equipment.

Growing acceptance of category 6 cable is one of the main trends in the industry. Before, category 5 and improved category 5e UTP cables had been favored for data applications. Though, new applications necessitate cables with high performance that can deliver superior bandwidth and a high rate of data transfer. Particularly, there was a necessity to decrease both signal attenuation and alien crosstalk amid cable pairs to accommodate the obligation of cutting-edge applications like gigabit ethernet, where four cable pairs are used to communicate data instantaneously. The category 6 cable comes to terms with these necessities with a larger copper conductor to decrease signal reduction between receiver and transmitter.

Because of the increasing demand for a connected workplace, increasing penetration of BYOD, the evolution of the OTT industry, and increasing cybersecurity spending, the demand for networking equipment is on the rise in the APAC region.

Read More: https://www.psmarketresearch.com/market-analysis/apac-networking-equipment-marketConnected Workplace has A Lot to do with the Increasing Demand for Networking Equipment in the APAC The APAC networking equipment market will have significant growth in the years to come. This is because of the factors like increasing bandwidth requirements and mounting data traffic. Additionally, rising incidents of cyber-attacks are also pushing the demand for networking equipment where organizations are obligated to accept networking security solutions so as to alleviate risks ascending from this kind of attack. The industry is considered into routers, security devices, switches, modems, cables, storage devices, access points, repeaters, bridges, NIC, and others including amplifiers, antennas, and hubs. Of these, routers had the maximum demand in the past. Furthermore, momentous demand for high-speed data transmission from clients has permitted large enterprises to improve network competence at reduced working costs, which will improve the growth prospects for routers in the future. Repeaters with speeds above 300 Mbps will have the largest share in the years to come. Furthermore, the demand for these will exhibit the fastest growth in the near future. This is a result of the requirement of incessant availability of robust network and internet connectivity in administrations in addition to consumers. An unmanaged switch will hold a larger revenue share in the near future. Though, managed switches will register faster growth in the coming years. This is a result of the fact that managed switches bid better control as compared to the data access authorization, and has the aptitude to arrange, accomplish, and monitor the LAN. The initial funding is in managed switches as opposed to unmanaged switches, but large enterprises prefer managed switches because of their improved quality of security and service. The growing hospitality sector is posing a prospect for the APAC networking equipment market. Japan and India are posting healthy development in hospitality sector. Currently, Wi-Fi in hotels is not a luxury facility anymore. As Wi-Fi connection is a vital part of contemporary lifestyle, many guests are seeing the attendance of Wi-Fi facility as a part of their policymaking process whilst confirming reservations. Consequently, increasing the hospitality sector would surge the requirement for networking equipment. Growing acceptance of category 6 cable is one of the main trends in the industry. Before, category 5 and improved category 5e UTP cables had been favored for data applications. Though, new applications necessitate cables with high performance that can deliver superior bandwidth and a high rate of data transfer. Particularly, there was a necessity to decrease both signal attenuation and alien crosstalk amid cable pairs to accommodate the obligation of cutting-edge applications like gigabit ethernet, where four cable pairs are used to communicate data instantaneously. The category 6 cable comes to terms with these necessities with a larger copper conductor to decrease signal reduction between receiver and transmitter. Because of the increasing demand for a connected workplace, increasing penetration of BYOD, the evolution of the OTT industry, and increasing cybersecurity spending, the demand for networking equipment is on the rise in the APAC region. Read More: https://www.psmarketresearch.com/market-analysis/apac-networking-equipment-market0 Comments ·0 Shares ·909 Views ·0 Reviews -

Next-Generation Firewall Market To Demonstrate a CAGR of 11.9% during 2020–2025

Factors such as the increasing number of cyber threats, rising adoption of the bring-your-own-device (BYOD) policy in workplaces, limitations of traditional firewall, surging implementation of the internet of things (IoT), and rising number of financial organizations across the globe are expected to drive the growth of the next-generation firewall (NGFW) market at a CAGR of 11.9% during the forecast period (2020–2025). According to P&S Intelligence, the market size will increase from $2,706.9 million in 2019 to $5,188.8 million by 2025. Moreover, the market is witnessing a trend of surging adoption of IoT technology.

One of the major factors aiding the market growth is the increasing cases of cyber threats. For instance, about 2.9 million cases of cybercrime were reported in the U.S. in 2018. Thus, the requirement of cyber-attack prevention solution in the current business landscape is surging. NGFW is a security solution that can be easily combined with the existing technologies in a company’s network to enhance security and data breach protection and provide comprehensive network visibility. This technology is also effective in preventing intrusion, protecting the cloud, and offering application awareness and control.

The enterprise size segment of the next-generation firewall industry is bifurcated into large enterprises and small and medium enterprises (SMEs). Between the two, the large enterprises category accounted for the larger share in the market in 2019, owing to the increasing requirement for enhanced digital security solutions to manage and secure vast amounts of data in big companies. On the other hand, the SMEs category is projected to observe the higher CAGR during the forecast period, due to the increasing focus of such companies on deploying the cost-effective NGFW solutions.

Moreover, based on the industry segment, the next-generation firewall market is classified into banking, financial services, and insurance (BFSI); aerospace & defense; government & public utility; information technology (IT) & telecommunication; retail; healthcare; manufacturing; and others. Among these, the BFSI industry generated the highest market revenue in 2019. This is ascribed to the surging adoption of digital technologies, rising number of financial institutions, and increasing need to prevent cyberattacks. Whereas, the healthcare industry is projected to observe the highest CAGR during the forecast period, owing to the increasing cases of data breach in the sector.

Geographically, the next-generation firewall industry in the Asia-Pacific (APAC) region is expected to witness the highest CAGR during the forecast period. This can be ascribed to the rising number of SMEs, surging demand for IoT devices, increasing cases of cyber threats, and growing focus of governments on data security, in the region. Whereas, North America held the largest market share in 2019, owing to the presence of a large number of market players, rising adoption of cloud solutions, and growing initiatives of governments for the safety of public data.

Thus, the rising number of cyberattacks and the increasing number of financial institutions across the globe are expected to propel the market growth during the forecast period.

Read More: https://www.psmarketresearch.com/market-analysis/next-generation-firewall-marketNext-Generation Firewall Market To Demonstrate a CAGR of 11.9% during 2020–2025 Factors such as the increasing number of cyber threats, rising adoption of the bring-your-own-device (BYOD) policy in workplaces, limitations of traditional firewall, surging implementation of the internet of things (IoT), and rising number of financial organizations across the globe are expected to drive the growth of the next-generation firewall (NGFW) market at a CAGR of 11.9% during the forecast period (2020–2025). According to P&S Intelligence, the market size will increase from $2,706.9 million in 2019 to $5,188.8 million by 2025. Moreover, the market is witnessing a trend of surging adoption of IoT technology. One of the major factors aiding the market growth is the increasing cases of cyber threats. For instance, about 2.9 million cases of cybercrime were reported in the U.S. in 2018. Thus, the requirement of cyber-attack prevention solution in the current business landscape is surging. NGFW is a security solution that can be easily combined with the existing technologies in a company’s network to enhance security and data breach protection and provide comprehensive network visibility. This technology is also effective in preventing intrusion, protecting the cloud, and offering application awareness and control. The enterprise size segment of the next-generation firewall industry is bifurcated into large enterprises and small and medium enterprises (SMEs). Between the two, the large enterprises category accounted for the larger share in the market in 2019, owing to the increasing requirement for enhanced digital security solutions to manage and secure vast amounts of data in big companies. On the other hand, the SMEs category is projected to observe the higher CAGR during the forecast period, due to the increasing focus of such companies on deploying the cost-effective NGFW solutions. Moreover, based on the industry segment, the next-generation firewall market is classified into banking, financial services, and insurance (BFSI); aerospace & defense; government & public utility; information technology (IT) & telecommunication; retail; healthcare; manufacturing; and others. Among these, the BFSI industry generated the highest market revenue in 2019. This is ascribed to the surging adoption of digital technologies, rising number of financial institutions, and increasing need to prevent cyberattacks. Whereas, the healthcare industry is projected to observe the highest CAGR during the forecast period, owing to the increasing cases of data breach in the sector. Geographically, the next-generation firewall industry in the Asia-Pacific (APAC) region is expected to witness the highest CAGR during the forecast period. This can be ascribed to the rising number of SMEs, surging demand for IoT devices, increasing cases of cyber threats, and growing focus of governments on data security, in the region. Whereas, North America held the largest market share in 2019, owing to the presence of a large number of market players, rising adoption of cloud solutions, and growing initiatives of governments for the safety of public data. Thus, the rising number of cyberattacks and the increasing number of financial institutions across the globe are expected to propel the market growth during the forecast period. Read More: https://www.psmarketresearch.com/market-analysis/next-generation-firewall-market0 Comments ·0 Shares ·882 Views ·0 Reviews -

North America Is Dominating Cloud OSS BSS Market

The total value of the cloud OSS BSS market was USD 20,502 million in 2022, and it will rise at a growth rate of above 12.0% shortly, reaching USD 50,762 million by 2030, according to P&S Intelligence.

This growth can be credited to the increasing requirement to decrease CAPEX, the growing demand for convergent billing arrangements, the rising placement of revenue management systems (RMSs), and the rising acceptance of 5G technology.

Growths in 5G technology support mechanizing industrial processes with the aid of machine-type communication armed with mobile broadband ability. Moreover, with the placement of 5G, the virtualization of network functionality aids several businesses and private operators to share their network range and functionality, which primes to low prices of facilities.

The requirement for RMSs is growing because of their features including credit limit, management of invoicing, charging, and payment. Also, this convergent billing arrangement provides an incorporated channel to new businesses for rating and valuing.

Through this, clientele can screen spending and instantaneous consumption through a specific service or transaction model. Therefore, service offers are accepting RMSs to aid retail, wholesale, and other firm business segments.

Additionally, the growth in the requirement to centralize individual arrangements will boost the application of RMSs and will back to the development of requirements for cloud OSS BSS solutions.

The IT and telecom category is projected to grow at the highest pace, of approximately 13%, in the coming few years. Telecom service workers can make money out of their businesses with the aid of cloud OSS BSS solutions.

The end-to-end business and workings including managing network performance, new item delivery, fault and billing problems, inventory, and client experience can be enhanced and monitored utilizing end-to-end cloud solutions.

The small and medium enterprise category is projected to grow at the highest pace, of approximately 12.3%, in the coming few years. Small and medium-sized enterprises play very vital roles in each community. As per a research article, approximately 400 million SMEs are working throughout the globe, which has recorded for 99% of worldwide establishments.

SMEs are making a lot of work opportunities, creating up to 60–85% of employment. As per the International Labor Organization, SMEs generated up to 70% of the global GDP.

North America is dominating the cloud OSS BSS market. This can be credited to the existence of key industry companies and the growth in digital businesses and arrangements in the continent. Furthermore, with the rising requirement to attain operational effectiveness and enormous competition among service workers, telecom workers are more intensive on the monetization of mobile broadband information services.

Hence, the increasing requirement to decrease CAPEX, the growing demand for convergent billing arrangements, the rising placement of revenue management systems (RMSs), and the rising acceptance of 5G technology are the major factors contributing to the growth of the cloud OSS BSS market.

Read More: https://www.psmarketresearch.com/market-analysis/cloud-oss-bss-marketNorth America Is Dominating Cloud OSS BSS Market The total value of the cloud OSS BSS market was USD 20,502 million in 2022, and it will rise at a growth rate of above 12.0% shortly, reaching USD 50,762 million by 2030, according to P&S Intelligence. This growth can be credited to the increasing requirement to decrease CAPEX, the growing demand for convergent billing arrangements, the rising placement of revenue management systems (RMSs), and the rising acceptance of 5G technology. Growths in 5G technology support mechanizing industrial processes with the aid of machine-type communication armed with mobile broadband ability. Moreover, with the placement of 5G, the virtualization of network functionality aids several businesses and private operators to share their network range and functionality, which primes to low prices of facilities. The requirement for RMSs is growing because of their features including credit limit, management of invoicing, charging, and payment. Also, this convergent billing arrangement provides an incorporated channel to new businesses for rating and valuing. Through this, clientele can screen spending and instantaneous consumption through a specific service or transaction model. Therefore, service offers are accepting RMSs to aid retail, wholesale, and other firm business segments. Additionally, the growth in the requirement to centralize individual arrangements will boost the application of RMSs and will back to the development of requirements for cloud OSS BSS solutions. The IT and telecom category is projected to grow at the highest pace, of approximately 13%, in the coming few years. Telecom service workers can make money out of their businesses with the aid of cloud OSS BSS solutions. The end-to-end business and workings including managing network performance, new item delivery, fault and billing problems, inventory, and client experience can be enhanced and monitored utilizing end-to-end cloud solutions. The small and medium enterprise category is projected to grow at the highest pace, of approximately 12.3%, in the coming few years. Small and medium-sized enterprises play very vital roles in each community. As per a research article, approximately 400 million SMEs are working throughout the globe, which has recorded for 99% of worldwide establishments. SMEs are making a lot of work opportunities, creating up to 60–85% of employment. As per the International Labor Organization, SMEs generated up to 70% of the global GDP. North America is dominating the cloud OSS BSS market. This can be credited to the existence of key industry companies and the growth in digital businesses and arrangements in the continent. Furthermore, with the rising requirement to attain operational effectiveness and enormous competition among service workers, telecom workers are more intensive on the monetization of mobile broadband information services. Hence, the increasing requirement to decrease CAPEX, the growing demand for convergent billing arrangements, the rising placement of revenue management systems (RMSs), and the rising acceptance of 5G technology are the major factors contributing to the growth of the cloud OSS BSS market. Read More: https://www.psmarketresearch.com/market-analysis/cloud-oss-bss-market0 Comments ·0 Shares ·789 Views ·0 Reviews -

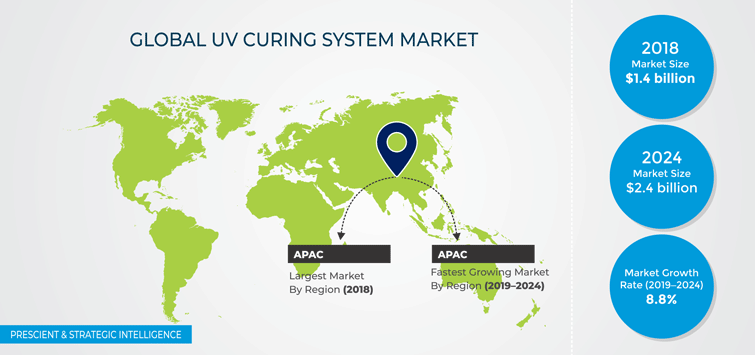

Packaging Industry Will Drive the Ultraviolet Curing System Market

The ultraviolet (UV) curing system market is experiencing growth, as per the report by market research company P&S Intelligence. The industry growth is due to the thriving demand for automobiles, healthcare devices, and consumer electronics.

The increasing acceptance of UV curing systems in furniture production units is observed as a market trend in the current scenario. Such systems are extensively utilized for the purpose of curing the coatings on numerous substrates, including wood, for high-standard finishing and fast drying, leading to better productivity.

Additionally, UV-cured coatings provide protection to substrates from external agents, including, accidental chemical spills, moisture, and corrosion. credited to such belongings, these systems are progressively accepted in manufacturing plants.

The extensive use of UV curing for packaging is one of the major drivers of the industry growth. Such systems are being installed in the food and beverage industry due to they are best for coating, printing, and adhesive applications, wherein product quality and safety are not compromised.

Key market players are, thus, concentrating on UV curing systems for the packaging of food because of the increasing consumption of processed food and beverages.

On the basis of segment type, the conveyor category generated the major revenue share in the past. Conveyor curing offers even ink curing due to the steady speed of the conveyor guarantees that every element is cured for the same period. This surges the quantity and simplifies the process of mass production.

The conventional UV category had the largest share in the past in the industry. Conventional UV systems can treat numerous kinds of substrates and provide different UV bandwidths for deeper-level curing. Because of such factors, the wide adoption of this technology in the food & beverage industry is increasing rapidly for packaging.

On the basis of the pressure segment, the medium category had the major share. Such systems are generally used for adhesion/bonding, glass decoration, varnishing, and printed circuit board curing.

The APAC region had a significant revenue share in the ultraviolet curing system market in the recent past. This can be credited to the substantial growth in the electronics and automotive sector and considerable demand for UV curing systems for wood, plastic, and metal finishing applications.

In addition, the growing demand for consumer electronics, such as PCBs, mainly because of the growing per-capita income of the people in the countries like Thailand, Vietnam, India, and Indonesia, is boosting the growth of the industry.

Hence, the increasing acceptance of UV curing systems in furniture production, and the growing per-capita income of people in numerous countries, will contribute to the growth of the industry in the years to come.

Read More: https://www.psmarketresearch.com/market-analysis/uv-curing-system-marketPackaging Industry Will Drive the Ultraviolet Curing System Market The ultraviolet (UV) curing system market is experiencing growth, as per the report by market research company P&S Intelligence. The industry growth is due to the thriving demand for automobiles, healthcare devices, and consumer electronics. The increasing acceptance of UV curing systems in furniture production units is observed as a market trend in the current scenario. Such systems are extensively utilized for the purpose of curing the coatings on numerous substrates, including wood, for high-standard finishing and fast drying, leading to better productivity. Additionally, UV-cured coatings provide protection to substrates from external agents, including, accidental chemical spills, moisture, and corrosion. credited to such belongings, these systems are progressively accepted in manufacturing plants. The extensive use of UV curing for packaging is one of the major drivers of the industry growth. Such systems are being installed in the food and beverage industry due to they are best for coating, printing, and adhesive applications, wherein product quality and safety are not compromised. Key market players are, thus, concentrating on UV curing systems for the packaging of food because of the increasing consumption of processed food and beverages. On the basis of segment type, the conveyor category generated the major revenue share in the past. Conveyor curing offers even ink curing due to the steady speed of the conveyor guarantees that every element is cured for the same period. This surges the quantity and simplifies the process of mass production. The conventional UV category had the largest share in the past in the industry. Conventional UV systems can treat numerous kinds of substrates and provide different UV bandwidths for deeper-level curing. Because of such factors, the wide adoption of this technology in the food & beverage industry is increasing rapidly for packaging. On the basis of the pressure segment, the medium category had the major share. Such systems are generally used for adhesion/bonding, glass decoration, varnishing, and printed circuit board curing. The APAC region had a significant revenue share in the ultraviolet curing system market in the recent past. This can be credited to the substantial growth in the electronics and automotive sector and considerable demand for UV curing systems for wood, plastic, and metal finishing applications. In addition, the growing demand for consumer electronics, such as PCBs, mainly because of the growing per-capita income of the people in the countries like Thailand, Vietnam, India, and Indonesia, is boosting the growth of the industry. Hence, the increasing acceptance of UV curing systems in furniture production, and the growing per-capita income of people in numerous countries, will contribute to the growth of the industry in the years to come. Read More: https://www.psmarketresearch.com/market-analysis/uv-curing-system-market0 Comments ·0 Shares ·1K Views ·0 Reviews -

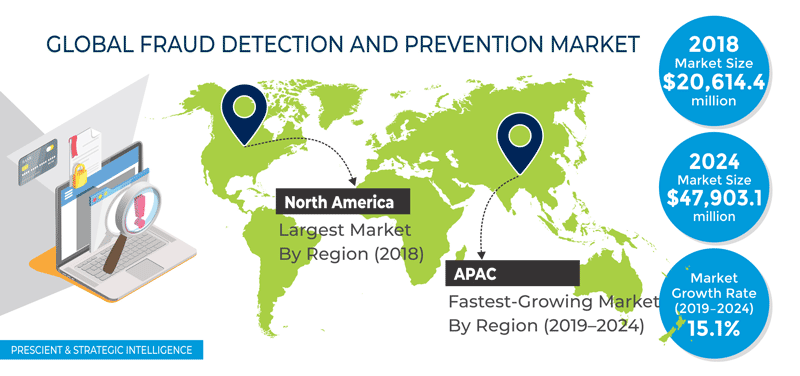

Fraud Detection and Prevention Market To Witness over $25,000.0-Million Growth by 2030

The strongest factors propelling the demand for fraud detection and prevention solutions are the rising adoption of artificial intelligence (AI) and machine learning (ML) to mitigate fraud, increasing need to counter mobile frauds, surging number of the elderly being phone-scammed, and escalating need to safeguard the online banking sector. Due to these factors, the fraud detection and prevention market value, which stood at $20,614.4 million in 2018, is projected to witness a 15.1% CAGR during 2019–2024 (forecast period, to reach $47,903.1 million by 2024.

Based on offering, the market is bifurcated into software and service, of which the software bifurcation held the larger share in 2018. This was due to the rising adoption of fraud analytics, governance, risk, and compliance (GRC), and authentication software by companies to mitigate cyber fraud and adhere to the data protection rules of governments. During the forecast period, the higher CAGR will be witnessed by the service bifurcation. With the increasing adoption of fraud detection and prevention solutions, the demand for various managed and professional services is rising too.

The bifurcations of the deployment type segment of the fraud detection and prevention market are on-premises and cloud-based. During the historical period (2014–2018), the market was dominated by the cloud-based bifurcation, which is also expected to witness the faster growth till 2024. Compared to on-premises deployment, cloud deployment is cheaper, as it eliminates the need to procure expensive hardware and maintain on-site servers. Moreover, the cloud allows users to track their operations in real time and scale up or down the data storage capacity without much effort.

Presently, hybrid approaches are trending in the fraud detection and prevention market, as they integrate various aspects of the process into one solution. Such an approach integrates multiple aspects of a potential fraud, analyzes each aspect as an individual malicious activity, and detects known, complex, unknown, and associative link patterns. Additionally, hybrid solutions involve the usage of rule-based algorithms, improved data integration, anomaly detection, social media analysis (SMA), and predictive modeling tools for a more-effective detection and prevention of frauds.

The major fraud detection and prevention market driver is the burgeoning number of mobile frauds around the world. Compared to 30% in 2018, 49% of all the risky transactions that took place around the world in 2019 were carried out via mobile phones. Scammers are using mobile emulators on their PCs and laptops to mimic a range of Android- and iOS-based mobile phones. These emulators allow users to breach the basic device recognition software by mimicking different mobile device software and hardware functionalities, thus making effective fraud detection and prevention solutions necessary.

A key opportunity area for the fraud detection and prevention market players is the usage of the blockchain technology for this purpose in supply chain. As the supply chain involves numerous stages of production, people, technologies, and the products themselves, it becomes an easy target for fraudsters. Therefore, companies are using blockchains, which are difficult to manipulate without the agreement of all the stakeholders. Blockchains also allow the products to be traced through the entire process, beginning from the procurement of raw materials to the delivery of the final product.

In 2018, North America was the largest fraud detection and prevention market owing to the rapid adoption of the cloud technology by small and large companies, which is enabling fraudsters to target them. Moreover, technological advancements and the integration of the internet of things (IoT) in such solutions will drive the regional market. The fastest growth during the forecast period will be seen in Asia-Pacific (APAC) due to the swift economic prosperity, increasing number of large companies, advancing IT sector, surging popularity of cloud computing, and stringent government data protection laws.

Hence, with the rapid digitization leading to the rising number of cyber frauds, the demand for solutions that can detect and prevent such mishaps will continue to burgeon.

Read More: https://www.psmarketresearch.com/market-analysis/fraud-detection-and-prevention-market

Fraud Detection and Prevention Market To Witness over $25,000.0-Million Growth by 2030 The strongest factors propelling the demand for fraud detection and prevention solutions are the rising adoption of artificial intelligence (AI) and machine learning (ML) to mitigate fraud, increasing need to counter mobile frauds, surging number of the elderly being phone-scammed, and escalating need to safeguard the online banking sector. Due to these factors, the fraud detection and prevention market value, which stood at $20,614.4 million in 2018, is projected to witness a 15.1% CAGR during 2019–2024 (forecast period, to reach $47,903.1 million by 2024. Based on offering, the market is bifurcated into software and service, of which the software bifurcation held the larger share in 2018. This was due to the rising adoption of fraud analytics, governance, risk, and compliance (GRC), and authentication software by companies to mitigate cyber fraud and adhere to the data protection rules of governments. During the forecast period, the higher CAGR will be witnessed by the service bifurcation. With the increasing adoption of fraud detection and prevention solutions, the demand for various managed and professional services is rising too. The bifurcations of the deployment type segment of the fraud detection and prevention market are on-premises and cloud-based. During the historical period (2014–2018), the market was dominated by the cloud-based bifurcation, which is also expected to witness the faster growth till 2024. Compared to on-premises deployment, cloud deployment is cheaper, as it eliminates the need to procure expensive hardware and maintain on-site servers. Moreover, the cloud allows users to track their operations in real time and scale up or down the data storage capacity without much effort. Presently, hybrid approaches are trending in the fraud detection and prevention market, as they integrate various aspects of the process into one solution. Such an approach integrates multiple aspects of a potential fraud, analyzes each aspect as an individual malicious activity, and detects known, complex, unknown, and associative link patterns. Additionally, hybrid solutions involve the usage of rule-based algorithms, improved data integration, anomaly detection, social media analysis (SMA), and predictive modeling tools for a more-effective detection and prevention of frauds. The major fraud detection and prevention market driver is the burgeoning number of mobile frauds around the world. Compared to 30% in 2018, 49% of all the risky transactions that took place around the world in 2019 were carried out via mobile phones. Scammers are using mobile emulators on their PCs and laptops to mimic a range of Android- and iOS-based mobile phones. These emulators allow users to breach the basic device recognition software by mimicking different mobile device software and hardware functionalities, thus making effective fraud detection and prevention solutions necessary. A key opportunity area for the fraud detection and prevention market players is the usage of the blockchain technology for this purpose in supply chain. As the supply chain involves numerous stages of production, people, technologies, and the products themselves, it becomes an easy target for fraudsters. Therefore, companies are using blockchains, which are difficult to manipulate without the agreement of all the stakeholders. Blockchains also allow the products to be traced through the entire process, beginning from the procurement of raw materials to the delivery of the final product. In 2018, North America was the largest fraud detection and prevention market owing to the rapid adoption of the cloud technology by small and large companies, which is enabling fraudsters to target them. Moreover, technological advancements and the integration of the internet of things (IoT) in such solutions will drive the regional market. The fastest growth during the forecast period will be seen in Asia-Pacific (APAC) due to the swift economic prosperity, increasing number of large companies, advancing IT sector, surging popularity of cloud computing, and stringent government data protection laws. Hence, with the rapid digitization leading to the rising number of cyber frauds, the demand for solutions that can detect and prevent such mishaps will continue to burgeon. Read More: https://www.psmarketresearch.com/market-analysis/fraud-detection-and-prevention-market0 Comments ·0 Shares ·1K Views ·0 Reviews -

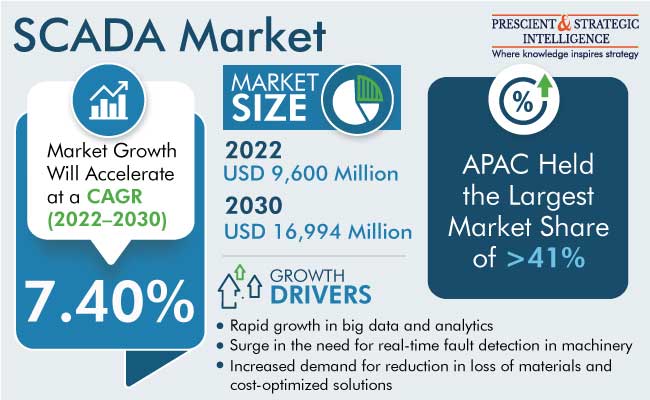

SCADA Market Will Reach USD 16,994 Million by 2030

The total value of the global SCADA market was USD 9,600 million in 2022, and it will rise at a growth rate of above 7.4% shortly, reaching USD 16,994 million by 2030, according to P&S Intelligence.

This growth can be credited to the high acceptance of Industry 4.0 solutions utilizing SCADA devices, the rising usage of software platforms including artificial intelligence and the Internet of Things, the growing requirement for industrial mobility solutions for better procedure management, and the growing advancements in wireless sensor networks (WSNs).

Artificial intelligence and the Internet of Things have enhanced the processes of numerous sectors. On the basis of different world statistics, the count of devices linked to IoT networks is quickly growing.

Through the usage of SCADA arrangements, the IoT is altering manufacturing facilities by joining a huge network of smart systems. IoT and AI-based arrangements allow industries to control and screen their developments and applications, precisely forecast machine failure, and attain quicker response times, thus growing effectiveness and reducing operational prices.

Furthermore, by utilizing IoT and AI, information is gathered, analyzed, and utilized for rising predictive models, which can help in making work well-organized and lead to augmented incomes for a company. In order to modernize plant processes, IoT and AI-based SCADA platforms streamline data transmission and study.

The surge in the rise of Industry 4.0 for both process industries and manufacturing industries quickens industry development. They utilize such facilities as part of their digitalization strategies.

Because of their high level of technology adoption, industries are witnessing a high requirement to update the present SCADA system. Therefore, the need for these systems has been growing, mainly because of the digitization of manufacturing processes via the usage of sensors and data devices.

In the coming few years, the hardware category is projected to advance at the highest development rate, of approximately 7.8%. This can be credited to the high requirement for components such as RTU, HMI, and PLC in industrial processes and mechanization solutions to attain the targets of scalability, efficiency, and growth in the manufacturing sector.

Furthermore, progressive hardware advances the performance of systems, accountable for process mechanization, and delivers valued data. Therefore, the industry’s key players employed technologies for the growth of HMI and progressive PLCs, which can work with diverse SCADA solutions.

In recent years, North America held the major revenue share in the worldwide SCADA market. This is mainly because of the steady energy management of SCADA, huge expenditure on technologies, the increasing industrial sector, and the rising acceptance of automation technology.

Hence, the high acceptance of Industry 4.0 solutions utilizing SCADA devices, the rising usage of software platforms including artificial intelligence and the Internet of Things, and the growing requirement for industrial mobility solutions for better procedure management are the major factors propelling the SCADA market.

Read More: https://www.psmarketresearch.com/market-analysis/scada-market

SCADA Market Will Reach USD 16,994 Million by 2030 The total value of the global SCADA market was USD 9,600 million in 2022, and it will rise at a growth rate of above 7.4% shortly, reaching USD 16,994 million by 2030, according to P&S Intelligence. This growth can be credited to the high acceptance of Industry 4.0 solutions utilizing SCADA devices, the rising usage of software platforms including artificial intelligence and the Internet of Things, the growing requirement for industrial mobility solutions for better procedure management, and the growing advancements in wireless sensor networks (WSNs). Artificial intelligence and the Internet of Things have enhanced the processes of numerous sectors. On the basis of different world statistics, the count of devices linked to IoT networks is quickly growing. Through the usage of SCADA arrangements, the IoT is altering manufacturing facilities by joining a huge network of smart systems. IoT and AI-based arrangements allow industries to control and screen their developments and applications, precisely forecast machine failure, and attain quicker response times, thus growing effectiveness and reducing operational prices. Furthermore, by utilizing IoT and AI, information is gathered, analyzed, and utilized for rising predictive models, which can help in making work well-organized and lead to augmented incomes for a company. In order to modernize plant processes, IoT and AI-based SCADA platforms streamline data transmission and study. The surge in the rise of Industry 4.0 for both process industries and manufacturing industries quickens industry development. They utilize such facilities as part of their digitalization strategies. Because of their high level of technology adoption, industries are witnessing a high requirement to update the present SCADA system. Therefore, the need for these systems has been growing, mainly because of the digitization of manufacturing processes via the usage of sensors and data devices. In the coming few years, the hardware category is projected to advance at the highest development rate, of approximately 7.8%. This can be credited to the high requirement for components such as RTU, HMI, and PLC in industrial processes and mechanization solutions to attain the targets of scalability, efficiency, and growth in the manufacturing sector. Furthermore, progressive hardware advances the performance of systems, accountable for process mechanization, and delivers valued data. Therefore, the industry’s key players employed technologies for the growth of HMI and progressive PLCs, which can work with diverse SCADA solutions. In recent years, North America held the major revenue share in the worldwide SCADA market. This is mainly because of the steady energy management of SCADA, huge expenditure on technologies, the increasing industrial sector, and the rising acceptance of automation technology. Hence, the high acceptance of Industry 4.0 solutions utilizing SCADA devices, the rising usage of software platforms including artificial intelligence and the Internet of Things, and the growing requirement for industrial mobility solutions for better procedure management are the major factors propelling the SCADA market. Read More: https://www.psmarketresearch.com/market-analysis/scada-market0 Comments ·0 Shares ·1K Views ·0 Reviews -

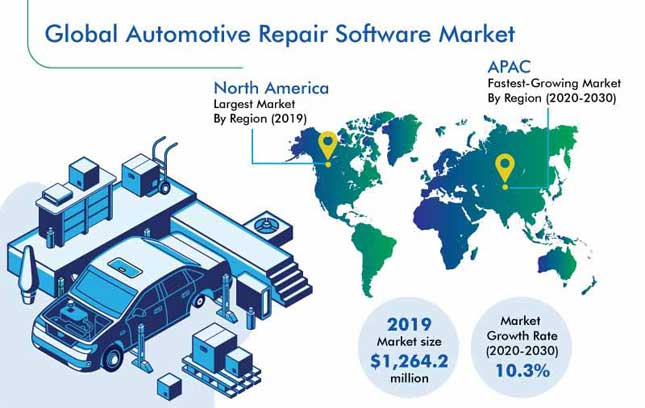

Automotive Repair Software Market to Register 10.3% CAGR during 2020–2030

Because of increasing the disposable income, rapid urbanization, swift economic growth in emerging economies, and technological advancements, the number of vehicles on roads has risen significantly on roads all across the globe. For example, approximately 91.3 million motor vehicles were sold worldwide in 2019. Over the last ten years, the affordability of vehicles has increased considerably. Moreover, due to technological advancements autonomous and connected cars have also started emerging in the markets. Owing to this surging number of vehicles on roads, the number of auto repair shops has also taken a hike.

The smooth functioning of vehicles depends a lot upon their proper maintenance. If a vehicle is not maintained on a regular basis, it is highly likely that its functioning will take a hit. Therefore, auto repair shops are of great importance to the automotive industry. Now that the number of vehicles has risen, the operations and processes in these shops have also become more complex. There is a growing need for improving efficiency, which is why several auto repair shops are making use of auto repair software. This software is capable of automating the day-to-day aspects of managing an auto repair shop, thereby simplifying the operational processes.

Attributed to these reasons, the global automotive repair software market generated revenue of $1,264.2 million in 2019 and is predicted to advance at a 10.3% CAGR during the forecast period (2020–2030). Maintenance, repair, and service are the major kinds of this software, among which, the demand for repair solutions is expected to be the highest in the coming years. This is because of the increased adoption of auto repair software for automobile repair and diagnostics. These solutions provide valuable insights from colored diagram for wiring, experienced technicians, and repair information provided by the automaker for ease of understanding.

This being said, the demand for automotive repair software is also projected to rise for service offerings in the near future. This can be ascribed to the fact that several service centers are making use of this software for shop management services, with the goal of saving time, increasing productivity, and increasing efficiency. The major end users of automotive repair software are manufacturer/original equipment manufacturer retail store, automotive repair workshop, auto parts wholesaler, and automotive dealer. Automotive repair workshops made the most use of this software, owing to the fact that a large number of such independent automobile servicing shops exist across the globe.

North America has been the major user of automotive repair software in the past, which is on account of the rising average age of vehicles in the region. Regular servicing is important for vehicles that are owned for a longer time in order to extract optimum mileage out of them, which is why various auto repair shops are adopting this software for increasing efficiency. In addition to this, due to the fact that Asia-Pacific account for the major number of vehicles in operation, the region is projected to emerge as the fastest growing automotive repair software market.

Hence, the demand for automotive repair software is rising due to the growing number of vehicles on roads and increasing number of auto repair shops.

Read More: https://www.psmarketresearch.com/market-analysis/automotive-repair-software-market

Automotive Repair Software Market to Register 10.3% CAGR during 2020–2030 Because of increasing the disposable income, rapid urbanization, swift economic growth in emerging economies, and technological advancements, the number of vehicles on roads has risen significantly on roads all across the globe. For example, approximately 91.3 million motor vehicles were sold worldwide in 2019. Over the last ten years, the affordability of vehicles has increased considerably. Moreover, due to technological advancements autonomous and connected cars have also started emerging in the markets. Owing to this surging number of vehicles on roads, the number of auto repair shops has also taken a hike. The smooth functioning of vehicles depends a lot upon their proper maintenance. If a vehicle is not maintained on a regular basis, it is highly likely that its functioning will take a hit. Therefore, auto repair shops are of great importance to the automotive industry. Now that the number of vehicles has risen, the operations and processes in these shops have also become more complex. There is a growing need for improving efficiency, which is why several auto repair shops are making use of auto repair software. This software is capable of automating the day-to-day aspects of managing an auto repair shop, thereby simplifying the operational processes. Attributed to these reasons, the global automotive repair software market generated revenue of $1,264.2 million in 2019 and is predicted to advance at a 10.3% CAGR during the forecast period (2020–2030). Maintenance, repair, and service are the major kinds of this software, among which, the demand for repair solutions is expected to be the highest in the coming years. This is because of the increased adoption of auto repair software for automobile repair and diagnostics. These solutions provide valuable insights from colored diagram for wiring, experienced technicians, and repair information provided by the automaker for ease of understanding. This being said, the demand for automotive repair software is also projected to rise for service offerings in the near future. This can be ascribed to the fact that several service centers are making use of this software for shop management services, with the goal of saving time, increasing productivity, and increasing efficiency. The major end users of automotive repair software are manufacturer/original equipment manufacturer retail store, automotive repair workshop, auto parts wholesaler, and automotive dealer. Automotive repair workshops made the most use of this software, owing to the fact that a large number of such independent automobile servicing shops exist across the globe. North America has been the major user of automotive repair software in the past, which is on account of the rising average age of vehicles in the region. Regular servicing is important for vehicles that are owned for a longer time in order to extract optimum mileage out of them, which is why various auto repair shops are adopting this software for increasing efficiency. In addition to this, due to the fact that Asia-Pacific account for the major number of vehicles in operation, the region is projected to emerge as the fastest growing automotive repair software market. Hence, the demand for automotive repair software is rising due to the growing number of vehicles on roads and increasing number of auto repair shops. Read More: https://www.psmarketresearch.com/market-analysis/automotive-repair-software-market0 Comments ·0 Shares ·797 Views ·0 Reviews -

Why will Asia-Pacific Data Center Infrastructure Management Market Boom in Future?

The global data center infrastructure management (DCIM) market generated a revenue of $1.5 billion in 2020 and it is set to exhibit rapid expansion from 2020 to 2030 (forecast period), as per the estimates of the market research company, P&S Intelligence. The market is being driven by the burgeoning requirement for gaining end-to-end visibility to predict capacity management requirements, rising focus on improving energy efficiency and data center uptime, soaring need for a low carbon footprint and sustainability, and surging number of hyperscale data centers across the world.

Enterprises must plan their data center strategy in such a way that the systems never breakdown. Moreover, data center managers must make sure that their data center strategy can cope with the evolving needs of organizations. DCIM provides insights and visibility by monitoring several parameters, such as security uptime, network operations, and the performance of computers and data center servers, and addressing network issues when they arise. Thus, DCIM assists organizations in improving their decision-making process and data center managers in improving the uptime of data centers.

Depending on application, the DCIM market is divided into capacity planning, environmental monitoring, asset management, power monitoring, and business intelligence (BI) and analytics categories. Out of these, the asset management category is predicted to dominate the market in the coming years. This is ascribed to the fact that data centers are becoming highly complex in nature and the use of traditional methods, such as spreadsheets, pen, and paper cannot assist in tracking the performance of assets. Moreover, an average error rate of 15% should be expected when using these obsolete processes.

When deployment model is taken into consideration, the market is classified into cloud and on-premises. Of these, the on-premises category is predicted to hold larger share in the upcoming years. DCIM systems collect data from various sensors and monitor infrastructure availability, humidity, power consumption, temperature, and airflow and thus, play a critical role for enterprises. Globally, the Asia-Pacific (APAC) region is expected to be the fastest-growing region in the DCIM market in the years to come.

This will be because of the implementation of government policies aimed at facilitating data center construction, adoption of advanced technologies, such as the internet of things (IoT) and machine learning, and surge in the data center business in the region. For example, the Indian government’s Data Center policy, which was released in 2020, intends to make India a global data center hub by encouraging investments in the sector, supporting the development of trusted hosting infrastructure in order to meet the escalating customer requirements, and ensuring the delivery of state-of-the-art services to citizens.

Thus, the demand for DCIM services will soar in the coming years, mainly because of the rising requirement for improving the uptime and efficiency of data centers, growing need for gaining end-to-end visibility to predict capacity management requirements, and mushrooming number of hyperscale data centers all over the world.

Read More: https://www.psmarketresearch.com/market-analysis/data-center-infrastructure-management-dcim-marketWhy will Asia-Pacific Data Center Infrastructure Management Market Boom in Future? The global data center infrastructure management (DCIM) market generated a revenue of $1.5 billion in 2020 and it is set to exhibit rapid expansion from 2020 to 2030 (forecast period), as per the estimates of the market research company, P&S Intelligence. The market is being driven by the burgeoning requirement for gaining end-to-end visibility to predict capacity management requirements, rising focus on improving energy efficiency and data center uptime, soaring need for a low carbon footprint and sustainability, and surging number of hyperscale data centers across the world. Enterprises must plan their data center strategy in such a way that the systems never breakdown. Moreover, data center managers must make sure that their data center strategy can cope with the evolving needs of organizations. DCIM provides insights and visibility by monitoring several parameters, such as security uptime, network operations, and the performance of computers and data center servers, and addressing network issues when they arise. Thus, DCIM assists organizations in improving their decision-making process and data center managers in improving the uptime of data centers. Depending on application, the DCIM market is divided into capacity planning, environmental monitoring, asset management, power monitoring, and business intelligence (BI) and analytics categories. Out of these, the asset management category is predicted to dominate the market in the coming years. This is ascribed to the fact that data centers are becoming highly complex in nature and the use of traditional methods, such as spreadsheets, pen, and paper cannot assist in tracking the performance of assets. Moreover, an average error rate of 15% should be expected when using these obsolete processes. When deployment model is taken into consideration, the market is classified into cloud and on-premises. Of these, the on-premises category is predicted to hold larger share in the upcoming years. DCIM systems collect data from various sensors and monitor infrastructure availability, humidity, power consumption, temperature, and airflow and thus, play a critical role for enterprises. Globally, the Asia-Pacific (APAC) region is expected to be the fastest-growing region in the DCIM market in the years to come. This will be because of the implementation of government policies aimed at facilitating data center construction, adoption of advanced technologies, such as the internet of things (IoT) and machine learning, and surge in the data center business in the region. For example, the Indian government’s Data Center policy, which was released in 2020, intends to make India a global data center hub by encouraging investments in the sector, supporting the development of trusted hosting infrastructure in order to meet the escalating customer requirements, and ensuring the delivery of state-of-the-art services to citizens. Thus, the demand for DCIM services will soar in the coming years, mainly because of the rising requirement for improving the uptime and efficiency of data centers, growing need for gaining end-to-end visibility to predict capacity management requirements, and mushrooming number of hyperscale data centers all over the world. Read More: https://www.psmarketresearch.com/market-analysis/data-center-infrastructure-management-dcim-market0 Comments ·0 Shares ·957 Views ·0 Reviews -

Why Does 24–44 Age Group Account for Largest Mobile Gaming Market Share?

In 2021, the mobile gaming market stood at $93,163.8 million, which is on the path to reaching a size of $261,586.3 million in 2030. The market is predicted to advance at a CAGR of 12.2% from 2021 to 2030, owing to the growing mobile usage and increasing acceptance of innovative technologies. Furthermore, the rising e-sports popularity will pave the way for a booming market. In addition, the access to higher data speeds would increase with the extensive use of the 5G technology, thus leading to a widening gaming audience.

Smartphones are playing a crucial role in the expansion of the global gaming market. This market is attaining scalability owing to the development of mobile games. The count of gamers is increasing tremendously with the rising disposable income of consumers, thus consequently driving their purchasing power, which enables them to buy smartphones. For instance, social media platforms, such as Instagram and Facebook, are deploying mobile games to enhance their advertising and marketing strategies.

The increasing adoption of technological advancements is leading to the mobile gaming market expansion. Cloud gaming is changing the gaming industry by providing better opportunities for game developers. A number of technological businesses and cloud gamers have accepted cloud gaming since it minimizes the memory space required to unlock the game on smartphones. Additionally, AR uses audio and video in a more-realistic setting, which captivates users. Furthermore, through a first viewpoint accompanied by a 360-degree vision, VR offers an extraordinary real-world experience to users. For instance, Pokémon Go and Ingress are among the widely searched AR games on app stores.

The adoption of a freemium business model is expected to advance at a mobile gaming market CAGR of over 10% from 2021 to 2030. Freemium games offer an additional benefit of making in-game purchases. The basic version of a freemium game is available for free; however, the player must pay for additional features or level upgrades. The payment can be made as per the preferences of gamers, as there are various payment mechanisms.

The largest share in the mobile gaming market was held by the 24–44 years age group in 2021. This may be attributed to the rapid adaptation to technical advances by this age bracket. Since this age group has people who are tech-savvy and keen to try new products, a major chunk of smartphone users lie in this category. The release of new smartphones with special features facilitates an enhanced user experience, which drives the mobile game downloads by this age group.

APAC will be a significant contributor to the mobile gaming market, owing to the increasing sale of smartphones, coupled with the bettering internet connectivity. The regional middle-class population is not only technologically sophisticated but also richer than before, which makes the region an appropriate investment hotspot. Moreover, India is on the path of promoting its beliefs and values through games. For instance, the Indian government, in collaboration with IIT Bombay, is planning to develop a center of excellence in gaming to boost the nation’s mobile gaming companies.

The skyrocketing demand for smartphone games and the popular gaming campaign #PlayApartTogether supported by WHO during COVID-19 have led to aggressive product development in this market.

Read More: https://www.psmarketresearch.com/market-analysis/mobile-gaming-marketWhy Does 24–44 Age Group Account for Largest Mobile Gaming Market Share? In 2021, the mobile gaming market stood at $93,163.8 million, which is on the path to reaching a size of $261,586.3 million in 2030. The market is predicted to advance at a CAGR of 12.2% from 2021 to 2030, owing to the growing mobile usage and increasing acceptance of innovative technologies. Furthermore, the rising e-sports popularity will pave the way for a booming market. In addition, the access to higher data speeds would increase with the extensive use of the 5G technology, thus leading to a widening gaming audience. Smartphones are playing a crucial role in the expansion of the global gaming market. This market is attaining scalability owing to the development of mobile games. The count of gamers is increasing tremendously with the rising disposable income of consumers, thus consequently driving their purchasing power, which enables them to buy smartphones. For instance, social media platforms, such as Instagram and Facebook, are deploying mobile games to enhance their advertising and marketing strategies. The increasing adoption of technological advancements is leading to the mobile gaming market expansion. Cloud gaming is changing the gaming industry by providing better opportunities for game developers. A number of technological businesses and cloud gamers have accepted cloud gaming since it minimizes the memory space required to unlock the game on smartphones. Additionally, AR uses audio and video in a more-realistic setting, which captivates users. Furthermore, through a first viewpoint accompanied by a 360-degree vision, VR offers an extraordinary real-world experience to users. For instance, Pokémon Go and Ingress are among the widely searched AR games on app stores. The adoption of a freemium business model is expected to advance at a mobile gaming market CAGR of over 10% from 2021 to 2030. Freemium games offer an additional benefit of making in-game purchases. The basic version of a freemium game is available for free; however, the player must pay for additional features or level upgrades. The payment can be made as per the preferences of gamers, as there are various payment mechanisms. The largest share in the mobile gaming market was held by the 24–44 years age group in 2021. This may be attributed to the rapid adaptation to technical advances by this age bracket. Since this age group has people who are tech-savvy and keen to try new products, a major chunk of smartphone users lie in this category. The release of new smartphones with special features facilitates an enhanced user experience, which drives the mobile game downloads by this age group. APAC will be a significant contributor to the mobile gaming market, owing to the increasing sale of smartphones, coupled with the bettering internet connectivity. The regional middle-class population is not only technologically sophisticated but also richer than before, which makes the region an appropriate investment hotspot. Moreover, India is on the path of promoting its beliefs and values through games. For instance, the Indian government, in collaboration with IIT Bombay, is planning to develop a center of excellence in gaming to boost the nation’s mobile gaming companies. The skyrocketing demand for smartphone games and the popular gaming campaign #PlayApartTogether supported by WHO during COVID-19 have led to aggressive product development in this market. Read More: https://www.psmarketresearch.com/market-analysis/mobile-gaming-market0 Comments ·0 Shares ·1K Views ·0 Reviews -

Why Will the Solutions Category Generate Higher Revenue in Intelligent Process Automation Market?

The major drivers in the global intelligent process automation market are the surging deployment of AI and robotic process automation in numerous corporations all around the world. In 2021, $10,801.5 million were generated by the sale of these solutions, which is set to touch $31,377.0 million by 2030. Moreover, the market will grow at a 12.6% CAGR from 2021 to 2030. Furthermore, the rising adoption of technologically advanced devices will open the closed opportunities for market players, who can advance and modify their solutions to suit the customer needs prevailing in the present scenario.

Within the offering segment, the intelligent process automation market can be bifurcated into service and solution categories. The latter bifurcation will grow at the fastest CAGR, accounting for about 14.8% in the coming years. This can be primarily attributed to the surging application of intelligent process automation (IPA) solutions in numerous industries, which in turn, will increase workflow efficiency. Apart from making the processes efficient in SMEs and large corporations, these IPA solutions not only are economic but also save the time invested in business workflows and process execution.

When segmented on application, IT operations rule the intelligent process automation market. This can be ascribed to the surging deployment of DL, AI, and ML to carry on important tasks, including managing customer requirements and attaining greater insights into the willingness to purchase of consumers by adopting IT systems. Moreover, the dynamic consumer needs are addressed by RPOA and AI together, which encourage companies to adopt IPA. Nonetheless, the application management category will also not lag and witness an approximately 13.0% CAGR in the coming years because of the highly-competitive market.

Under the organization segment, the SMEs bifurcation, which presently accounts for a significant usage of these programs, will grow at the higher CAGR, of approximately 15.1%. This is because of the increasing utilization of these solutions in SMEs for an enhanced production process so that voluminous data can be managed by smaller units. Additionally, this innovation is becoming increasingly popular in SMEs because of the enhanced operational performance offered by IPA.

In 2021, the BFSI sector dominated the intelligent process automation market, accounting for about 30% market share. This is because of the rising integration of IPA to safeguard sensitive data in a digitalized era and consumer services. These interfaces are controlled and monitored by IPA solutions to guarantee that transactions occur properly and those workflow inefficiencies are removed. Furthermore, BFSI organizations are assisted by RPA in modernizing their operational processes by interfacing with old systems via bot deployment. Therefore, all of these will together augment growth in the market.

Geographically, APAC is to dominate the intelligent process automation market in the coming years. Sales of these solutions in APAC will fetch market players a combined $13,473.1 million by 2030, advancing at the highest CAGR of approximately 14.6% in the future period. This is because of the swift deployment of innovations. Furthermore, numerous nations in the region are implementing IPA platforms to strengthen the firm foundations of their position in the entire circular economy.

Hence, the surging deployment of AI and robotic process automation in numerous corporations drive the market.

Read More: https://www.psmarketresearch.com/market-analysis/intelligent-process-automation-market

Why Will the Solutions Category Generate Higher Revenue in Intelligent Process Automation Market? The major drivers in the global intelligent process automation market are the surging deployment of AI and robotic process automation in numerous corporations all around the world. In 2021, $10,801.5 million were generated by the sale of these solutions, which is set to touch $31,377.0 million by 2030. Moreover, the market will grow at a 12.6% CAGR from 2021 to 2030. Furthermore, the rising adoption of technologically advanced devices will open the closed opportunities for market players, who can advance and modify their solutions to suit the customer needs prevailing in the present scenario. Within the offering segment, the intelligent process automation market can be bifurcated into service and solution categories. The latter bifurcation will grow at the fastest CAGR, accounting for about 14.8% in the coming years. This can be primarily attributed to the surging application of intelligent process automation (IPA) solutions in numerous industries, which in turn, will increase workflow efficiency. Apart from making the processes efficient in SMEs and large corporations, these IPA solutions not only are economic but also save the time invested in business workflows and process execution. When segmented on application, IT operations rule the intelligent process automation market. This can be ascribed to the surging deployment of DL, AI, and ML to carry on important tasks, including managing customer requirements and attaining greater insights into the willingness to purchase of consumers by adopting IT systems. Moreover, the dynamic consumer needs are addressed by RPOA and AI together, which encourage companies to adopt IPA. Nonetheless, the application management category will also not lag and witness an approximately 13.0% CAGR in the coming years because of the highly-competitive market. Under the organization segment, the SMEs bifurcation, which presently accounts for a significant usage of these programs, will grow at the higher CAGR, of approximately 15.1%. This is because of the increasing utilization of these solutions in SMEs for an enhanced production process so that voluminous data can be managed by smaller units. Additionally, this innovation is becoming increasingly popular in SMEs because of the enhanced operational performance offered by IPA. In 2021, the BFSI sector dominated the intelligent process automation market, accounting for about 30% market share. This is because of the rising integration of IPA to safeguard sensitive data in a digitalized era and consumer services. These interfaces are controlled and monitored by IPA solutions to guarantee that transactions occur properly and those workflow inefficiencies are removed. Furthermore, BFSI organizations are assisted by RPA in modernizing their operational processes by interfacing with old systems via bot deployment. Therefore, all of these will together augment growth in the market. Geographically, APAC is to dominate the intelligent process automation market in the coming years. Sales of these solutions in APAC will fetch market players a combined $13,473.1 million by 2030, advancing at the highest CAGR of approximately 14.6% in the future period. This is because of the swift deployment of innovations. Furthermore, numerous nations in the region are implementing IPA platforms to strengthen the firm foundations of their position in the entire circular economy. Hence, the surging deployment of AI and robotic process automation in numerous corporations drive the market. Read More: https://www.psmarketresearch.com/market-analysis/intelligent-process-automation-market0 Comments ·0 Shares ·922 Views ·0 Reviews -

Rising Industrialization and Urbanization giving Rise to Increased Demand for GNSS Chips

The rising emphasis on the growth of smart cities is the main factor driving the GNSS chip market all around the world. The advance of smart cities denotes an urban development vision to integrate IoT technology and ICT in a secure means for managing the resources of the city in an effective manner. Rapid urbanization all around the world is leading to the snowballing focus on more sustainable kinds of cities.

Because of this, governments of numerous nations are more and more funding smart city projects. GNSS chips are utilized as a key enabler in smart city infra, in addition to in well-organized city planning and upkeep. Hence, the fast urbanization, in the company with the growing emphasis on the progress of smart cities, is responsible for the GNSS chip market growth.

The market is categorized into transport, automotive, consumer electronics, agriculture, construction, marine and military, and defense. Among all of these verticals, the automotive one has the largest demand in the GNSS chip market. As a result of the increasing technological improvements in connected vehicles, the need for GNSS-enabled applications and services in the automotive sector is constantly rising at a global level.

Smart Cities use big data and IoT for the exchange of digital info and communication for improvising the city services regarding performance, excellence, and well-being of citizens. The applications associated with Smart City are advanced keeping in mind the development of urban flow management. The number of people living in cities will be doubled by 2050. The urban population will reach six billion by 2050. This will surge the enormous pressure on the accessible resource

The GNSS chip market is categorized into, tablets, smartphones, PND, in-vehicle systems, and others. Among these, smartphones are the market dominator and will continue like this in the coming years as well. This has much to do with the increasing demand for smartphones, as a result of their falling prices in the global market, particularly in developing nations. The falling prices are directly responsible for the people buying more smartphones and thus propelling the demand for navigation chips.

The major companies in the GNSS chip market are focusing on the introduction of products and partnerships to increase their standing. Chip manufacturers are focusing more and more on strategic associations with tech providers to syndicate each other’s know-how and offer enhanced GNSS chips. The main market players include Broadcom Limited, Qualcomm Incorporated Intel Corporation, Skyworks Solutions Inc., Furuno Electric Co. Ltd., Quectel Wireless Solutions Co. Ltd., NXP Semiconductors, Navika Electronics, MediaTek Inc., and U-blox Holding AG.

The increasing demand for wearable and connected devices and electronics, and the growing requirement for accurate and instantaneous data are driving the demand for GNSS chip technology.

Read More: https://www.psmarketresearch.com/market-analysis/gnss-chip-marketRising Industrialization and Urbanization giving Rise to Increased Demand for GNSS Chips The rising emphasis on the growth of smart cities is the main factor driving the GNSS chip market all around the world. The advance of smart cities denotes an urban development vision to integrate IoT technology and ICT in a secure means for managing the resources of the city in an effective manner. Rapid urbanization all around the world is leading to the snowballing focus on more sustainable kinds of cities. Because of this, governments of numerous nations are more and more funding smart city projects. GNSS chips are utilized as a key enabler in smart city infra, in addition to in well-organized city planning and upkeep. Hence, the fast urbanization, in the company with the growing emphasis on the progress of smart cities, is responsible for the GNSS chip market growth. The market is categorized into transport, automotive, consumer electronics, agriculture, construction, marine and military, and defense. Among all of these verticals, the automotive one has the largest demand in the GNSS chip market. As a result of the increasing technological improvements in connected vehicles, the need for GNSS-enabled applications and services in the automotive sector is constantly rising at a global level. Smart Cities use big data and IoT for the exchange of digital info and communication for improvising the city services regarding performance, excellence, and well-being of citizens. The applications associated with Smart City are advanced keeping in mind the development of urban flow management. The number of people living in cities will be doubled by 2050. The urban population will reach six billion by 2050. This will surge the enormous pressure on the accessible resource The GNSS chip market is categorized into, tablets, smartphones, PND, in-vehicle systems, and others. Among these, smartphones are the market dominator and will continue like this in the coming years as well. This has much to do with the increasing demand for smartphones, as a result of their falling prices in the global market, particularly in developing nations. The falling prices are directly responsible for the people buying more smartphones and thus propelling the demand for navigation chips. The major companies in the GNSS chip market are focusing on the introduction of products and partnerships to increase their standing. Chip manufacturers are focusing more and more on strategic associations with tech providers to syndicate each other’s know-how and offer enhanced GNSS chips. The main market players include Broadcom Limited, Qualcomm Incorporated Intel Corporation, Skyworks Solutions Inc., Furuno Electric Co. Ltd., Quectel Wireless Solutions Co. Ltd., NXP Semiconductors, Navika Electronics, MediaTek Inc., and U-blox Holding AG. The increasing demand for wearable and connected devices and electronics, and the growing requirement for accurate and instantaneous data are driving the demand for GNSS chip technology. Read More: https://www.psmarketresearch.com/market-analysis/gnss-chip-market0 Comments ·0 Shares ·614 Views ·0 Reviews -

Telecom Cloud Market To Observe Fastest Growth In APAC

As per a report by P&S Intelligence, the telecom cloud market generated a value of USD 17.9 billion in 2022, and it will reach USD 92.6 billion, propelling at 22.80% CAGR, by 2030.

The growth of the industry is attributed to the increasing demand for robust network connectivity, growing usage of cloud-native environments, and rising 5G standards and IoT usage.

A major trend observed in the telecom cloud industry is the quick digital transformation in enterprises. Because of digitization, the progression of the way consumers and businesses interact has transformed their internal processes.

In 2022, the Software as a Service (SaaS) category, based on the service model, accounted for the largest telecom cloud market share, of 58%.

Platform as a Service (PaaS) has gained immense popularity due to its appeal to programmers who prioritize coding over infrastructure development and maintenance. By automating back-end processes and providing essential building blocks, PaaS empowers businesses to meet demand and elevate their success to new heights.

Additionally, PaaS proves to be highly beneficial for small industries and startups for several reasons. It offers cost-effectiveness and allows businesses to concentrate on their core expertise without the burden of maintaining foundational infrastructure.

The hybrid category, based on the deployment model, will observe the fastest growth, of approximately 24.5% CAGR, in the years to come. This is mainly credited to the requirement for both private and public clouds to support the environment of IT. The hybrid model enables businesses to constantly create their work environments on either the private or public cloud with no additional expenses for the infrastructure.

In 2022, the large enterprises category, based on organization size, accounted for the largest share in the industry, of 64%, owing to the mounting adoption of cloud solutions by multinational companies to manage the databases of large consumers.

The North American telecom cloud industry accounted for the largest industry share, of more than 36%, in 2022.

The APAC telecom cloud industry will witness the fastest growth, of more than 24% compound annual growth rate, in the years to come. This can be credited to the increasing expenditure on cloud infrastructure services in this region.